Business tips

How can spending limits for contactless payments affect your business?

Business tips

Accepting contactless payments is a great idea for your business, however it does mean dealing with the challenge of transaction limits. Consumers can only spend so much each time they use a contactless method and this may affect how much you’re able to benefit from adopting the technology.

Why do services limit contactless payment amounts?

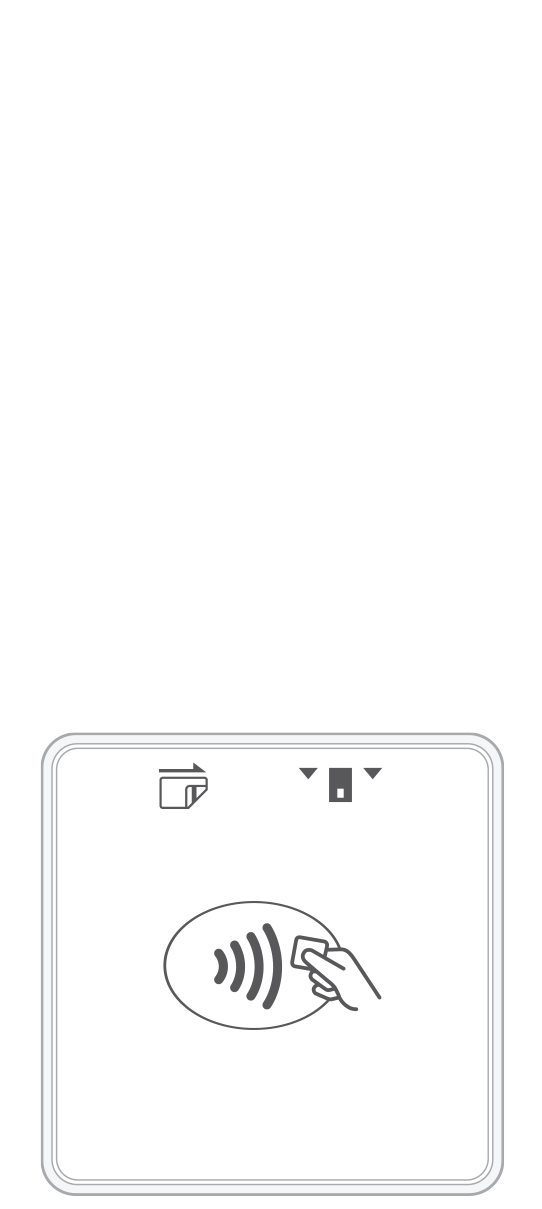

Contactless payments can be made using a credit card with a radio-frequency identification (RIFD) chip or a smartphone equipped with near-field communication (NFC) technology. Currently, only a handful of card issuers in the U.S. have contactless options, but most major cell phone providers offer mobile payments or mobile wallets.

Consumers love the speed and convenience these payments offer, but it’s because it’s such an easy way to pay that service providers put a cap on how much a person can spend at once. When your customers choose a contactless option, they can zip through the checkout line without signing or entering a PIN. This creates a greater level of risk, especially if the provider also offers a zero-liability policy to protect consumers from being held responsible for fraudulent purchases. Hence the need to safeguard these transactions through payment amount limits.

Contactless limits on the rise.

Having said that, spending limits are beginning to rise as more and more consumers make the switch to contactless payments. In the U.S., consumers can currently spend between $50 and $100 per transaction. The limit is much lower in the U.K., around $38, with 42 percent of consumers saying they’d like to be able to spend more.

This increasing demand bodes well for retailers, since it means customers who prefer contactless payment methods will be able to make larger purchases in a single visit. However, there is a concern regarding a potential rise in fraudulent activity. Higher spending limits may make obtaining payment information more attractive to malicious fraudsters, which could have a negative impact on consumers, businesses, and service providers.

Working within the limits.

Before investing in an NFC contactless payment scanner or RFID card reader, consider whether or not it will actually benefit your company. Right now, customers use contactless payments most often when buying groceries, restaurant meals, beverages, snacks, and clothes. If your business deals in these types of products, you could attract more customers by making a contactless option available. On the other hand, if you sell a lot of big-ticket items, or if the majority of your customers make large purchases, investing in contactless payment technology might not make as much sense.

Examine your sales history and customers’ buying habits and listen to what your customers are saying. High demand for a contactless option could trump the apparent logic of the numbers, especially if you offer a lot of items people tend to buy on impulse. It’s not uncommon for users of contactless payments to report spending more money or using their cards more frequently, simply because it’s so convenient.

Given the rising demand for contactless options and the relatively low cost of NFC contactless and RFID terminals, your business is likely to benefit from offering these payment methods even with the current spending limits in place.

More from Business tips

Start your Payanywhere account.

Start your Payanywhere account.

3-in-1 Reader |  Terminal |  Keypad |  PINPad Pro |  Flex |  POS+ | |

|---|---|---|---|---|---|---|

Payment types | ||||||

EMV chip card payments (dip) | ||||||

Contactless payments (tap) | ||||||

Magstripe payments (swipe) | ||||||

PIN debit + EBT | ||||||

Device features | ||||||

Built-in barcode scanner | ||||||

Built-in receipt printer | ||||||

Customer-facing second screen | ||||||

External pinpad | ||||||

Wireless use | ||||||

Network | ||||||

Ethernet connectivity | With dock | |||||

Wifi connectivity | ||||||

4G connectivity | ||||||

Pricing | ||||||

Free Placement | ||||||