Business tips

How Mobile Payments Can Change Your Business

News

Smartphones seem to be everywhere these days, and although it’s not quite true that “everyone” has one, it’s not much of a stretch – a study conducted by the Pew Research Center found that nearly two-thirds of Americans owned a smartphone in 2015, and 19 percent rely on their smartphones as their gateway to the internet and staying connected to the world. These numbers are expected to continue to grow, as are the capabilities of mobile technology, including using a mobile phone as a way to pay for goods and services via near-field communications (NFC) – a mobile wallet.

Smartphones seem to be everywhere these days, and although it’s not quite true that “everyone” has one, it’s not much of a stretch – a study conducted by the Pew Research Center found that nearly two-thirds of Americans owned a smartphone in 2015, and 19 percent rely on their smartphones as their gateway to the internet and staying connected to the world. These numbers are expected to continue to grow, as are the capabilities of mobile technology, including using a mobile phone as a way to pay for goods and services via near-field communications (NFC) – a mobile wallet.

Mobile wallets are essentially smartphone apps that store credit, debit and/or loyalty and prepaid card information so they can be used to pay for goods and services at retailers with NFC capabilities. They provide a faster, more secure checkout experience for customers than traditional magstripe and even the new chip-embedded EMV payment cards. Mobile payments have been around in one form or another for several years, but it’s only in the last couple of years that they’ve really taken off in the United States, thanks in part to the Apple Pay and Android Pay proprietary systems.

For business owners, mobile payments are more than just another “We Accept” sticker to put in your front window along with the Visa, MasterCard, American Express and Discover stickers. When you decide to accept mobile payments and integrate them into your marketing plan, you gain an invaluable tool to help increase your brand visibility and consumer loyalty, especially when tied to your own app, if you have one. Mobile payments offer customers a better way to shop, spend and save money, manage reward/loyalty programs and engage with their favorite and most frequented businesses. This, in turn, allows you to better manage your digital presence by targeting your customers with exclusive mobile incentives and coupons, and also to alert them to new and exciting merchandise and promotions. This relationship management is one of the reasons marketing plans exist in the first place, so if you are able to accept mobile payments, you definitely should consider doing so.

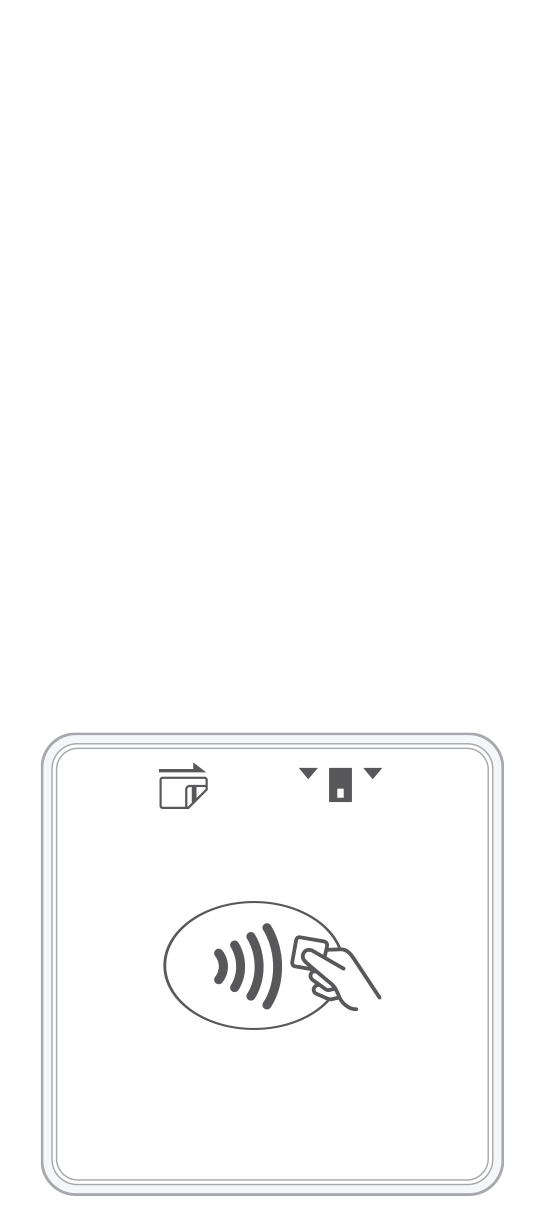

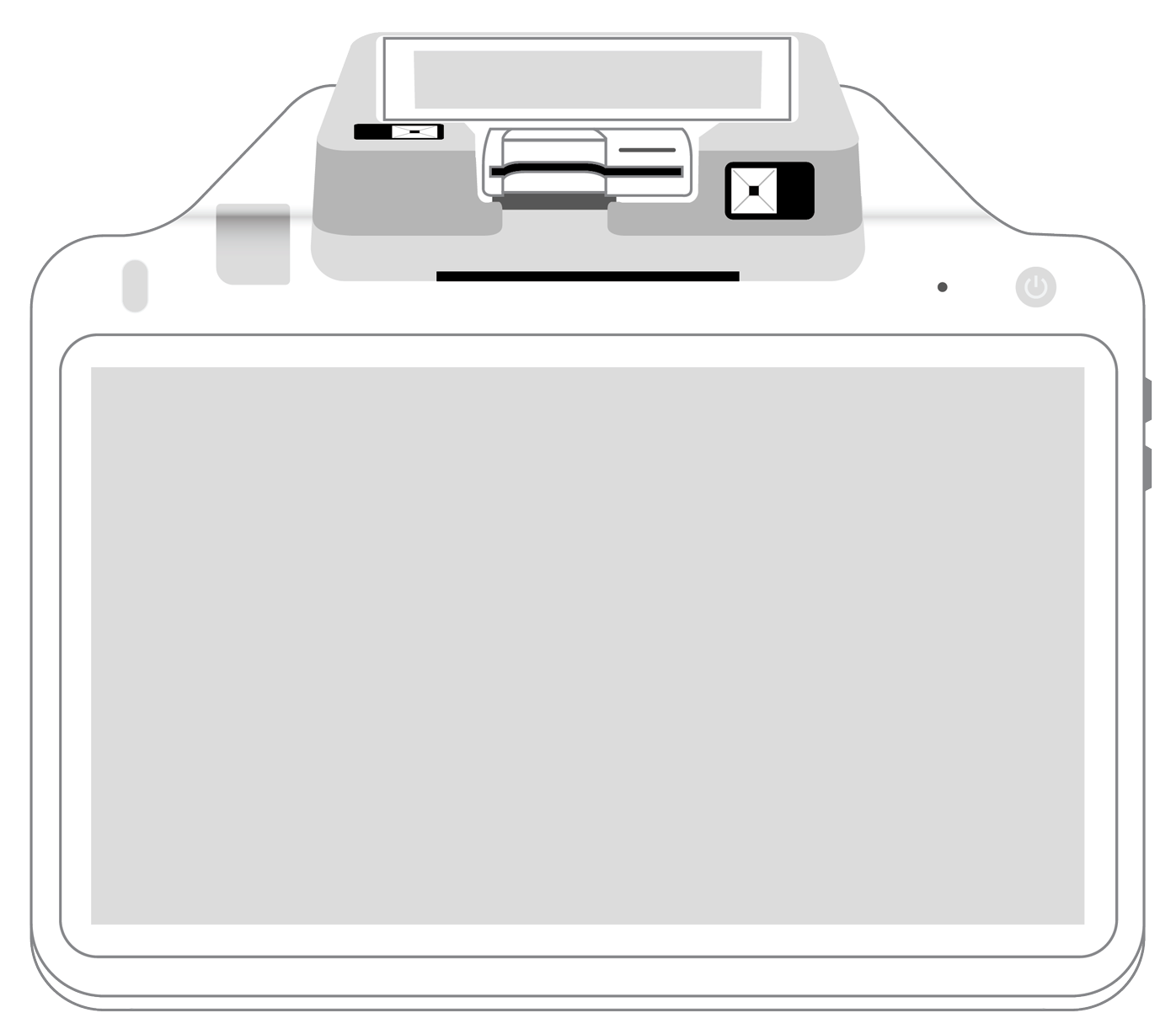

The three main players in the mobile payments space today are Apple, Google and Samsung, and all three systems use NFC technology to make payments. They work by the customer turning on the NFC function on her phone then tapping the phone on your NFC-enabled payment terminal. Samsung Pay also works with non-NFC terminals, as it has technology on its newest Galaxy phones that emulates the magnetic stripe on traditional credit and debit cards, which allows it to work on all terminals, whether they are set up for mobile payments or not.

Despite the increasing popularity, in order for mobile payments to go mainstream, it must be available everywhere customers shop, from the big box store on the corner of the two main streets in the city to the small coffee shop frequented by the locals. And that is where you, the merchant, comes in. Getting on board with mobile payments is as simple as ensuring your terminals are NFC capable. With the advent of EMV, which necessitated the purchase and installation of new payment terminals with the technology, many businesses are looking at and welcoming the new ways to pay, so it makes sense to make sure your new terminals also accept NFC payments.

The current trend of mobile wallets and mobile payments is not a flash in the pan – they are here to stay. Studies have shown that while slow to adopt, Americans are using mobile payments more than ever, and the numbers continue to increase. There are tangible advantages to businesses accepting mobile wallets from both a financial and marketing perspective, and getting in on this exciting new technology now can help set you apart from your competition, and be seen by your customers and business community as a forward-thinking business leader, ready to accept new technologies.

Start your Payanywhere account.

|  |  |  |  |  | |

|---|---|---|---|---|---|---|

Payment types | ||||||

EMV chip card payments (dip) | ||||||

Contactless payments (tap) | ||||||

Magstripe payments (swipe) | ||||||

PIN debit + EBT | ||||||

Device features | ||||||

Built-in barcode scanner | ||||||

Built-in receipt printer | ||||||

Customer-facing second screen | ||||||

External pinpad | ||||||

Wireless use | ||||||

Network | ||||||

Ethernet connectivity | With dock | |||||

Wifi connectivity | ||||||

4G connectivity | ||||||

Pricing | ||||||

Free Placement | ||||||